FuelEU Maritime represents a whole new level of regulatory complexity for the shipping industry, even as many are still grappling with the challenges of the EU ETS. But what is also new about FuelEU is that forward-leaning companies can actually benefit by cutting opex and even generating revenue through the compliance pooling option – and this will be determined by pooling prices.

The latest EU regulation, with implementation less than three months away, requires shipping companies to adopt unfamiliar metrics for bunkers, emissions and energy to measure the GHG intensity of their vessel operations, with well-to-wake emissions in CO2e equivalent and total energy usage – including shore power and wind – expressed in megajoules (MJ).

As well as these different parameters for analysis of carbon intensity, FuelEU introduces the new concept of compliance balances, with surpluses and deficits, that will entail various options including pooling, paying penalties for non-compliance, banking and borrowing.

Compliance balancing act

Compliance balances will be a crucial factor in determining the economic impact of FuelEU as companies seek to meet the initial 2% reduction in GHG intensity from a 2020 baseline of 91.16 CO2e/MJ to avoid the penalty of €2400 per tonne of VLSFOe. But they must also consider seemingly endless options, including vessel deployment and fuel selection, to optimise their commercial exposure.

Comparatively, the EU ETS, with issues such as opening of Union Registry accounts, getting access to EUAs and efficiently running the processes between owners, managers and charterers, now seems like a walk in the park!

Much industry attention is now focused on the potential benefits of the pooling option under FuelEU. So what does this entail?

When burning bunkers that have a GHG intensity below the threshold stipulated by the regulation, so-called ‘compliance surpluses’ are generated. This will be the case for either vessels burning LNG or LPG, or for those burning certain biofuels. Vessels burning conventional fossil fuels, on the other hand, will accumulate ‘compliance deficits’.

Stimulating low-carbon fuel uptake

The pooling mechanism, which is designed to stimulate uptake of low-carbon fuels, allows overcompliance by green-fuelled vessels to offset compliance deficits for ships burning fossil fuels and thereby generate overall compliance for the combined fleet of pooled vessels – owned as well as third-party vessels if these are included in such pools (not to be confused with commercial pools already familiar to the industry).

Through this mechanism, vessels generating a surplus can ‘sell’ this to those with compliance deficits. This means deficit-holders can avoid paying hefty penalties for exceeding the carbon intensity threshold, while those procuring the desired alternative fuels can actually generate additional revenues.

However, the price for selling and buying compliance balances in pools is not regulated, which has attracted criticism from quite a few industry players. Rather, it is left to the individual participants to agree pricing on a case-by-case basis.

If pooled internally within a single shipping company, pricing doesn’t matter much; the penalty avoided will be the benefit generated. But if pooling externally, the financial viability of the pooling strategy will depend on the price agreed for pooling surpluses with deficits.

OceanScore is using a market-based approach to discuss possible price ranges for pools. There are two main aspects: demand and supply of compliance surpluses and deficits, as well as a cost-based approach to identify upper and lower price limits (within these limits, demand and supply should move prices in an efficient market).

Supply and demand for surpluses

An in-depth analysis has been conducted by OceanScore of every vessel subject to FuelEU, the fuels burned and the resulting compliance balances per vessel. The results show the initial reduction target of 2% set by the EU has already been partly achieved and effectively reduced to 1.6%.

Most vessels still burn conventional fuels, resulting in a cumulative compliance deficit of 560k tonnes of VLSFOe for these vessels. Only a few hundred vessels, of which 85% are LNG and LPG carriers, generate surpluses, but these surplus volumes are substantial. Their cumulative compliance surplus comes in at 280k tonnes of VLSFOe, leaving a net industry gap of 280k tonnes.

When forecasting the demand-supply balance for compliance balances, what should be expected?

OceanScore data indicates the compliance market likely will be in balance (ie. the industry-wide threshold set by the EU will be met) already in 2025, based on contracts already entered into for biofuels. Surpluses generated by these operators as well as LNG/LPG carrier surpluses, will fuel the compliance pooling markets while at the same time reducing the industry’s compliance deficits. Voluntary emissions reduction schemes are expected to have an insignificant impact on the biofuel volumes used for pooling purposes.

This ample supply of compliance surpluses should prevent the pooling market being purely driven by scarcity of surpluses; prices will likely not be pushing the upper limit.

What is more, large operators – found mainly in container shipping and cruise, which have the highest exposure to FuelEU – will likely focus on securing neutral compliance balances for their fleets, at least initially, further reducing the compliance deficits, looking for external pooling options.

Penalty sets the upper price limit

To understand where pool prices will land, the cost of alternative courses of action – such as buying compliant bunkers, paying the penalty, banking and borrowing – needs to be analysed.

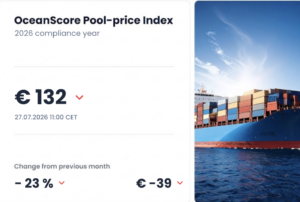

In short, no one will pool if the cost of doing so is above the penalty itself. The upper limit of pooling prices will therefore be defined by the €2400 penalty, minus some transaction cost and the extra effort to pool, resulting in a price of around €2300 per tonne of VLSFOe.

In a balanced market, the question is how low those offering compliance surpluses are willing to drop their prices. OceanScore has found that – especially if waste-based biofuels are used – trading compliance surpluses could still be viable at prices as low as €600 per tonne of VLSFOe.

Nevertheless, we should not expect pool prices to drop this low when introducing a dynamic component with the option to bank surpluses for future periods into the model.

Surplus-holders could expect that in 2030, after compliance thresholds are lowered, the demand for surpluses to pool will increase substantially, making surpluses scarce and met by substantial demand. If they assume that they could then commercialise their compliance surplus for say €2300 per tonne of VLSFOe, they might opt to bank their surplus rather than selling it ‘below value’. Given a 10% cost of capital, this would move the equilibrium price up to around €1400 per tonne, increasing towards 2030.

It can therefore be concluded that pooling prices over the next five years are likely to fluctuate between €1400 and €2300 per tonne of VLSFOe, which is a substantial price range.

Simulation of pool pricing scenarios

The ability to model different pool prices, which is a feature of OceanScore’s newly launched FuelEU Planner, is crucial for informed decision-making to optimise commercial benefits. The web-based tool also simulates different pooling, payment, banking and borrowing strategies, as well as the financial impact of bunker choices, alternative fuel investments, use of shore power and different deployment patterns.

Given fluctuating prices, moving fast to secure commercial agreements (formal agreements can only be finalised once the compliance balances have been verified in early 2026) for pool places at favourable conditions, depending on the perspective of surplus or deficit-holders, can be a significant lever on financial performance. And contractual agreements based on sound data need to be in place to cover risk, given tthat hird-party managers remain the Document of Compliance holders under FuelEU.

Focusing initially on fleet internal pooling is advisable, eliminating the uncertainties of the pooling market. It would be risky to assume there will be a rush of undercompliant vessels seeking to pool with surpluses towards the end of 2025.

Given the analytical complexities introduced by FuelEU, solid and granular simulation of different paths of action is of paramount importance. A deviation of just 0.5% in assessing a fleet’s GHG intensity or picking the wrong fuel can lead to wrong assumptions about one’s likely position in the pooling markets, with severe financial implications.

For more information contact:

Candice Buckle, Marketing Manager, OceanScore.

Email: candice.buckle@oceanscore.com

About OceanScore

Founded in 2020, OceanScore is a global provider of compliance and data solutions for the maritime industry with office locations in Germany, Poland, Portugal, and Singapore. Its suite of digital platforms and services is designed to support shipping to successfully navigate emissions regulation, facilitating the industry’s transformation towards sustainability. Beyond emissions, OceanScore tracks the sustainability, environmental, and reliability of over 130,000 vessels globally, serving the wider maritime ecosystem.