Liquefied natural gas (LNG) has been heralded by the EU as a greener alternative to conventional fuels for more than a decade, but it is only now that tangible commercial benefits are becoming available for shipping companies bunkering with LNG. Two regulations stand out: the inclusion of shipping into the EU Emissions Trading System (EU ETS) from last year and FuelEU Maritime that entered into force on January 1, 2025.

While both regulations complement each other and promote the use of cleaner fuels, they differ significantly in several aspects. And these must be understood in detail to secure comprehensive commercial optimization around the opportunities offered by the new regulatory environment.

Firstly, though, some notable similarities. Both regulations affect commercial vessels above 5,000GT. Both enforce full accountability for emissions in and between European ports, while providing discounts (normally 50%) for voyages between non-EU and EU ports. But there is a caveat with the more complex FuelEU discount scheme as the benefit may be higher than 50% for non-conventional fuels. Both regulations also take a phased approach, with emissions liability of 40% and 70% under the first two years of EU ETS, respectively, while FuelEU carbon intensity thresholds are tightened every five years until 2050.

Differing financial incentives

From a commercial perspective, the big difference lies in the way financial incentives are created through these regulations. EU ETS is a ‘pay as you pollute’ type of regulation: one EU Allowance (EUA), or carbon credit, must be procured per ton of CO2 emitted on a tank-to-wake basis and later surrendered to the European authorities.

FuelEU Maritime, on the other hand, defines an emissions threshold for each vessel subject to this regulation, based on the energy used within, or en route to/from, European waters measured in CO2e equivalent on a well-to-wake basis, thus including methane and nitrous oxide slip effects. Emissions above this threshold are subject to a substantial penalty, while emissions below it generate a compliance surplus that can be commercially utilized. Surpluses can be commercialized in different ways – either ‘banking’ them for use in future years or ‘pooling’ them with others that have a compliance deficit and want to avoid paying the penalty.

Compliance surplus with LNG

There are benefits from both regulations for vessels bunkering with LNG, which also is beneficial because of its higher calorific value (LCV). In relation to the EU ETS regime, LNG-fuelled vessels have emissions per metric tonne (MT) of 2.75MT, which is lower than that of around 3.2MT for those using conventional fuels.

When it comes to FuelEU Maritime, conventional fuels always generate deficits and thus the obligation to pay penalties, while LNG – depending on which type of engine is used – typically generates a significant surplus (emissions below threshold) that can be commercially utilized.

| MGO | LNG | |

| Volume (MT, LCV adjusted) | 1,000 | 870 |

| Cost of ETS (@€70/EUA, 70% phase-in) | 224,420 | 167,408 |

| FuelEU compliance balance (MT CO2e) | -61.07 | 566.02 |

| Potential FuelEU penalty (€) | 39.384 | – |

| Cost/Value if pooled (@€150/MT) | -9,160 | 84,903 |

| Total compliance cost (if pooled) (€) | 233,580 | 82,505 |

For LNG-fuelled vessels like LNG carriers, the story is clear: FuelEU generates benefits that partially offset the extra cost of EU ETS. But little else has changed from a competitive standpoint as everyone benefits the same way, though operational efficiency issues gain importance as there is a fuel cost add-on that must be considered.

The story is somewhat different for dual-fuel scenarios in which there is a real choice between different bunkers. The FuelEU Maritime regulation offers some interesting opportunities. In contrast to EU ETS, carbon factors differ significantly by engine type as methane and nitrous oxide slip are taken into consideration. The biggest benefits can be obtained with slow-speed diesel engines burning LNG.

Outweighing EU ETS savings

As a rule of thumb, EU ETS costs are roughly three to 3.5 times the cost of FuelEU penalties when burning conventional fuels. But it is a very different picture with LNG as this can result in FuelEU penalty savings outweighing EU ETS economies by a factor of 10x or more.

Furthermore, the different approach between both regulations when applying the 50% discount for voyages to/from the EU means savings on these legs can be fully utilized under FuelEU, making it a real booster for the use of LNG.

In a longer-term perspective, progressive reductions in FuelEU carbon intensity thresholds every five years will reduce the benefits of LNG until even slow-speed diesel engines burning LNG will cease to remain compliant in 2040. Commensurately, we can assume that the cost of EUAs under EU ETS will increase over time.

LNG will continue to provide benefits versus conventional fuels but will at some point start to be overtaken by biofuels, which will later give way to e-fuels – in line with the clear intent of the regulator to increase uptake of alternative fuels. Conventional LNG should therefore be treated as a transition fuel solution: it is fine for current operations but should be thoroughly assessed as a fuel option in making prospective fleet investment decisions.

Pooling opportunity

As well as reducing emissions under EU ETS, burning LNG on voyages yields a commercial benefit under FuelEU as it allows a compliance surplus to be generated that can potentially be monetized through the pooling system within the regulation.

This appears straightforward when pooling within a company’s own fleet – for example, running a couple of vessels on conventional bunkers and one on LNG – as long as compliance surpluses and deficits are roughly equivalent. But what about pooling with third-party vessels managed by another DOC holder? Those offering a surplus possibly generated through burning LNG will want to commercialize (ie. sell) this surplus.

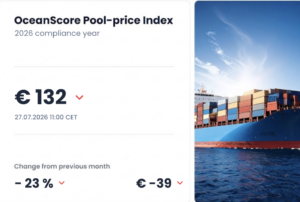

OceanScore analysis indicates that there will be an oversupply of surpluses available until at least 2030. As a result, these surpluses have been touted at low ‘prices’, to the degree that they are being offered at all. There are some surprising regional differences in prices being discussed, with prices in Asia at €150 or less per ton of CO2e and those in Europe at around €250 or less. If prices stabilize at these levels, those offering surpluses will have two options:

- Sell the surplus and take the cash.

- Bank the surplus and hope for better prices in the future.

As surpluses can be banked indefinitely, the latter is a viable option, especially as current pooling prices only reflect around 30% of the penalty that they help to avoid. That discount is way higher than the cost of capital for most shipping companies. A key consideration in this regard is liquidity needs, as well as the assumption that tightening of the FuelEU carbon intensity threshold in 2030 can lead to a scarcity of surpluses that will drive up prices for these to near penalty levels at around €650 per ton of CO2e.

Stakeholder alignment challenge

Even if a shipping company’s fleet manager has mastered the mechanics and math of FuelEU and defined a suitable strategy to smartly navigate the multiple options around fuel choices and pooling decisions, a third challenge still needs to be addressed: aligning this across all relevant stakeholders.

Surprisingly, the EU has allocated responsibility for FuelEU and related penalties to the DOC holder, while typically it’s the operator who decides which bunker to burn. Both are connected to the owner of the vessel through the respective Shipmans and charter parties. While integrated players are in a fortunate position, when the three roles are divided between different commercial entities, aligning incentives and timing of cash flows is a major challenge. In many cases, possible revenues gained from selling surpluses to pools will only be known when the pooling period is concluded – that is, April 30 of the year following the compliance period/year – based on the verified surplus volume and prevailing prices at the time. But bunkers needed to generate these surpluses are paid for at the time of bunkering.

There are therefore compounded timing, price and volume risks associated with surplus-related transactions that complicate alignment across stakeholders.

Capturing revenue upside

OceanScore is involved in a number of such discussions, supporting different stakeholders. Assuming a partnership-based, equitable approach is chosen, solid simulation of different deployment, voyage and bunker patterns is needed to make sure that any FuelEU clause – be it in Shipmans or charter parties – reflects the interests of all partners involved under all relevant scenarios. Given that the damage of a misaligned set of clauses can quickly be in the millions of US dollars, the extra effort invested in understanding the rules, their math and different options is well worth it.

While FuelEU offers potential for revenue upside from the use of LNG to reward the use of this fuel in the near future, making the most of this opportunity remains a challenge. But there is no need to leave money on the table.